.png)

The phone is still buzzing. One relative is asking what the doctor said. Another is asking what plan you have. You're trying to remember whether your insurance card says PPO, HMO, Medicare, or Medicaid, and at the same time someone has mentioned scans, biopsies, infusion drugs, and prior authorization.

That moment is where many people first start searching for insurance coverage for cancer patients. Not because they want to become experts in health insurance, but because treatment decisions suddenly feel tied to paperwork, phone calls, and deadlines.

If that's where you are today, take a breath. You do not need to figure out everything at once. Most insurance problems in cancer care become easier when you break them into smaller pieces: what plan you have, what treatment is being requested, whether your doctor is in network, whether the insurer needs approval first, and what to do if the answer is no.

Your First Step After a Cancer Diagnosis

A new diagnosis often creates two separate emergencies. The first is medical. The second is administrative. Patients tell me the insurance part can feel strangely urgent because it affects where they can go, how quickly they can start, and whether a recommended treatment will be covered.

A common early scenario looks like this. You leave an appointment with a folder full of notes, a pathology report you don't fully understand, and instructions to schedule more testing. Then someone says, “Call your insurance first.” That advice is frustrating, but it's often necessary.

The best first move is not to solve the whole insurance system in one day. It's to gather a small set of basics:

- Your insurance card

- Your member ID number

- The full name of your plan

- The name of the treating doctor or facility

- Any denial or approval letters you've already received

- A notebook or phone note for tracking calls

If your first oncology visit is coming up, it helps to know what will happen medically and administratively. This guide on what to expect at your first oncology appointment can make that first visit feel less unpredictable.

Bring both your questions and your paperwork. Patients who do that usually leave the visit with more clarity, even if every answer isn't available the same day.

What to focus on first

Try to answer three questions before you do anything else:

- What insurance do I have right now?

- Is my cancer doctor or infusion center in network?

- Does my planned testing or treatment need prior authorization?

That's enough to get started. You don't need to master all of oncology billing tonight. You just need a first foothold.

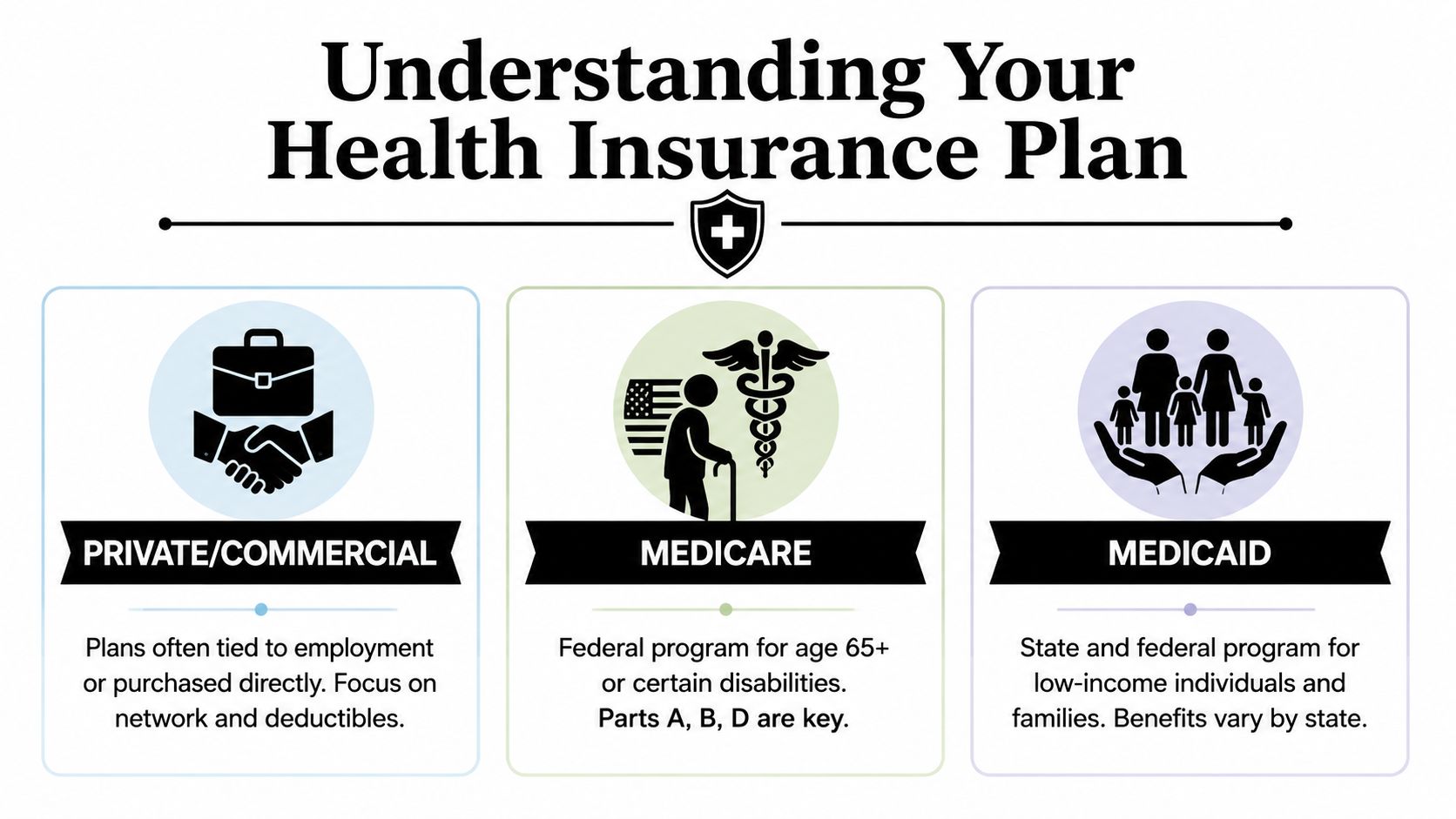

Understanding Your Health Insurance Plan

Many people think insurance is one big category. In practice, cancer care works very differently depending on whether you have private insurance, Medicare, or Medicaid.

The three main plan types

Think of these plans as three different rulebooks.

Private or commercial insurance is often tied to a job, a spouse's job, COBRA, or a plan you bought directly. These plans usually care a lot about network rules, deductibles, and whether a treatment meets the plan's medical policy.

Medicare is a federal program usually associated with age or disability. For cancer patients, the most important pieces are often:

- Part A, which relates to hospital care

- Part B, which often covers doctor visits, outpatient treatment, and many infused drugs

- Part D, which generally applies to many self-administered prescription medications

Medicaid is a state and federal program for people who qualify based on income and other eligibility rules. In cancer care, Medicaid can be a lifeline because it may open the door to diagnosis, specialist visits, and treatment that would otherwise be unaffordable.

A major policy difference matters here. Medicaid expansion under the ACA was linked to a sharp drop in uninsured rates for new cancer patients in expansion states, from 4.9% in 2010 to 2.1% in 2019, while non-expansion states only fell from 9.5% to 8.1% according to an American Cancer Society report on Medicaid expansion and cancer coverage. That matters in plain terms. Policy changes can affect whether patients reach care early or struggle to enter the system at all.

Comparing Insurance Types for Cancer Care

| Feature | Private/Commercial | Medicare | Medicaid |

|---|---|---|---|

| How people usually get it | Through an employer, spouse, COBRA, or direct purchase | Through age or qualifying disability | Through state eligibility rules tied to income and other factors |

| What to check first | Network, deductible, coinsurance, referral rules | Which parts you have, plus any supplement or Advantage plan | Managed care rules, participating providers, state-specific coverage details |

| Common cancer care issue | Out-of-network bills or prior authorization delays | Drug coverage split between medical and pharmacy benefits | Provider participation and approval processes |

| Best first phone question | “Is my oncologist and infusion site in network?” | “Is this drug billed under Part B or Part D?” | “Is this specialist enrolled with my plan, and does treatment need authorization?” |

The terms that confuse people most

A few terms cause trouble over and over.

- Deductible means what you may need to pay before the plan starts paying in full according to its rules.

- Copay is a set amount for a visit or service.

- Coinsurance is your share of the allowed cost.

- Network means the doctors, hospitals, and treatment centers your plan contracts with.

- Formulary is the plan's approved drug list, usually most important for oral cancer medicines and supportive medications.

Practical rule: Before you discuss bills, first identify the plan type. Many “billing problems” are actually network problems, pharmacy benefit problems, or prior authorization problems.

What New York patients should keep in mind

In New York City, many families move between plan types over time. A patient may start with employer coverage, lose work during treatment, shift to COBRA, then explore Medicaid or Medicare based on age or disability status. That isn't unusual.

The main thing is to stop guessing. Read the exact card. Call the member services number. Ask for a written explanation if a representative gives you a vague answer.

What Cancer Treatments Your Insurance May Cover

Once you know your plan type, the next question is simpler and harder at the same time: what exactly will this plan cover for my cancer care?

Most plans cover core parts of cancer treatment when they are medically necessary. That often includes office visits, labs, imaging, surgery, radiation, standard chemotherapy, and supportive care drugs. But modern oncology rarely stops at “standard chemotherapy.”

For many patients with advanced or treatment-resistant disease, the discussion may include:

- Immunotherapy

- Targeted therapy

- Low-dose chemotherapy regimens

- Biomarker or molecular testing

- Infusion-based supportive medications

Why newer treatments can trigger more scrutiny

Advanced treatments often require more documentation because insurers want to know why this treatment fits this cancer, this stage, and this patient. That doesn't always mean the treatment is inappropriate. It often means the insurer wants proof of medical necessity.

A frequent example is biomarker testing. Your oncologist may need those results to show why a targeted drug or immunotherapy makes sense. If the insurer denies the test, it can block the treatment decision downstream. This is one reason cancer insurance work can feel so circular. You need the test to justify the treatment, but you may need justification to get the test covered.

A 2024 analysis noted that 16.9% of new cancer cases relied on Medicaid and 4.4% were uninsured, and that even insured patients can still face denials for advanced treatments or necessary biomarker tests, especially in complex cancers like pancreatic or bile duct cancer, as described in the AACR discussion of the ACA's impact on access to cancer care.

What to ask when a treatment is proposed

When your doctor recommends a treatment, ask these questions in plain language:

- Is this billed as a medical benefit or a pharmacy benefit? Infused drugs and oral drugs can follow different rules.

- Do you need prior authorization before I start? If yes, ask who sends it and how you'll be updated.

- What diagnosis details support this choice? Histology, stage, and biomarker findings often matter.

- Could the plan label this investigational? If so, ask your doctor's office how they usually respond.

A realistic example

If a patient with advanced gastrointestinal cancer is considering an infusion treatment plus a low-dose regimen to reduce toxicity, the insurer may ask for pathology, prior treatment history, scan results, and notes explaining why that approach is appropriate now. That's normal.

The key is not to hear “more review” as “final no.” In cancer care, many treatment approvals depend on timing, documentation, and accurate coding.

Navigating Prior Authorizations and Network Rules

Two phrases cause more stress than almost anything else in oncology administration: prior authorization and out of network. They sound final, but they aren't.

A prior authorization is basically a permission process. Your insurer wants information before it agrees to pay for a service, scan, drug, or procedure. In oncology, this often applies to infusions, PET scans, genomic testing, and supportive medications.

What prior authorization really means

Patients often hear “we're waiting on authorization” and assume someone has already denied care. Sometimes that's not what happened. It may mean the insurer asked for:

- clinical notes

- pathology

- treatment history

- the planned drug and dosage

- the reason this treatment is being chosen now

That paperwork matters because access itself affects outcomes. A 2025 report on advanced melanoma found that newer immune therapies improved two-year survival to 46% for privately insured patients, compared with 28% for uninsured patients, underscoring how insurance status and navigating coverage rules shape real access to treatment, as summarized in this report on the JAMA study about insurance and melanoma survival.

A working checklist for patients

You can help your own authorization move faster if you ask focused questions.

Who is submitting it

Ask whether the oncologist's office, hospital, infusion center, or specialty pharmacy is responsible.What exactly is being requested

Get the treatment name, test name, or procedure name in writing if possible.When it was submitted

Dates matter. Write them down.What's still missing

Sometimes the delay is one pathology report, one office note, or one corrected diagnosis code.Where updates will appear

Some plans post status updates in a portal before anyone calls you.

If you want a plain-language look at workflow fixes behind the scenes, this article on improving patient access through better authorization management gives useful context for why oncology offices spend so much effort on these requests.

In network and out of network

Network status is a separate issue. A doctor can recommend the right treatment and still be out of network for your plan. That can affect what you owe or whether the plan pays at all.

If a specialist or infusion center you need isn't in network, ask about a network gap exception or single-case agreement. Those requests tell the insurer, “I need this provider because a suitable in-network option isn't realistically available for my situation.”

If a representative says “not covered,” ask the follow-up question immediately: “Do you mean not medically covered, or not covered at this provider because of network status?”

That one question can save days of confusion.

If you're also comparing locations for infusion care, this guide to finding a cancer infusion center near me can help you think through logistics, insurance fit, and treatment setup.

How to Appeal an Insurance Denial

A denial letter can feel like the floor dropped out from under you. Patients often read one sentence, stop breathing for a moment, and assume treatment is over. Usually, it isn't.

In cancer care, a denial is often the start of a process, not the end of one. Many denials happen because the insurer says the request lacked documentation, used the wrong pathway, or didn't yet show why the requested service was necessary for your exact diagnosis.

Read the denial for the real reason

Start by finding the denial category. It may be one of these:

- Not medically necessary

- Investigational or experimental

- Out of network

- No prior authorization

- Incomplete information

- Not a covered benefit under this plan

Each category points to a different next step. If the problem is incomplete information, the appeal may be straightforward. If it's a network issue, the office may need to request an exception. If it's medical necessity, your oncologist usually needs to provide a stronger explanation.

Research has shown why fighting for access matters. Uninsured patients have a relative risk of advanced-stage diagnosis ranging from 1.4 for breast cancer to 2.6 for melanoma compared with patients with private insurance, according to the NCBI review on insurance status and stage at diagnosis. Delayed access has consequences. That's why appeals are not “extra paperwork.” They are part of treatment access.

Build your appeal packet

A strong appeal usually includes several pieces working together.

The patient cover letter

Keep it brief and factual. Include:

- your name and member ID

- the denied service

- the date of denial

- the reason you're appealing

- a request for urgent review if treatment timing matters

The letter of medical necessity

This usually comes from the oncologist. It should explain:

- your diagnosis and stage

- what treatments you've already had

- why the requested treatment, scan, or test is appropriate now

- what could happen if care is delayed

The supporting records

Include the denial letter, clinic notes, pathology, scan reports, and any biomarker results relevant to the decision.

Keep a call log. Write down the date, time, phone number, representative name, and what was said after every insurance call.

Internal appeal and external appeal

Most plans have at least two levels.

An internal appeal asks the insurer to reconsider its own decision. An external appeal sends the dispute to an independent reviewer, depending on your plan and situation. If the denial involves urgent treatment, ask whether you qualify for an expedited review.

A practical consumer guide on how to challenge insurance company coverage decisions can help you organize the basic appeal steps and documents.

Many patients also benefit from hearing the appeal process explained out loud. This overview is a useful starting point:

Words you can use on the phone

If you freeze during insurance calls, use simple language:

- “I'm calling about a denial for cancer treatment and need the exact denial reason.”

- “Please tell me whether this is eligible for internal appeal, external review, or expedited review.”

- “What documents are missing, if any?”

- “Where should my doctor send the medical necessity letter?”

- “What is the deadline to appeal?”

Short, direct questions work better than long emotional explanations. You can be polite and firm at the same time.

Finding Financial Assistance in NYC

Insurance approval is only one part of the money problem. Even when treatment is covered, families may still face deductibles, copays, coinsurance, transportation costs, parking, missed work, and pharmacy bills. In New York City, the pace of care can make those costs hit fast.

A useful starting point is to ask the oncology office whether it has a financial counselor, social worker, or patient navigator who can screen for assistance programs. Those team members often know whether help is available for drug copays, transportation, lodging, or emergency household costs.

Where NYC patients can start

Begin with three buckets of help.

Hospital or clinic financial support

Ask whether there is charity care, payment assistance, or help with Medicaid applications or renewals.National cancer support organizations

Groups such as Patient Advocate Foundation and CancerCare may offer guidance or assistance programs depending on diagnosis, treatment, and funding availability.Local practical support

In NYC, transportation coordination, borough-based community organizations, and social work departments can sometimes help with rides, appointment logistics, and access to public benefits.

New York matters here because Medicaid plays a large role in cancer care. In 2019, Medicaid covered a significant share of new cancer cases, with state variation reaching as high as 37.9% in some areas, according to a Health Affairs Scholar analysis of insurance status at cancer diagnosis. For patients in Brooklyn, that means many oncology offices are used to working within NYS Medicaid rules, including infusion approvals and managed care requirements.

Questions to ask when money gets tight

Don't wait until bills pile up. Ask early:

- Can someone estimate my out-of-pocket responsibility?

- Is there manufacturer assistance for this drug?

- Can you check if I qualify for Medicaid or another public program?

- Do you know local help for transportation or non-medical expenses?

For a deeper list of options, this guide to cancer financial assistance is a good next step.

The best time to ask for financial help is before you miss a treatment, not after.

Preparing for Your Hirschfeld Oncology Consultation

A consultation is not just about hearing a treatment recommendation. It's also your chance to learn how the office handles the insurance side of complex care.

If you're seeking options for advanced disease, especially when treatment may involve immunotherapy, targeted drugs, or low-dose regimens, bring your insurance questions into the room. Patients sometimes hold those back because they don't want to “talk about money” during a medical visit. But coverage affects timing, feasibility, and stress. It belongs in the conversation.

Write your questions down in advance. Good ones include:

- How does your office handle prior authorizations for infusion treatments?

- If my plan denies a recommended therapy, who helps with the appeal?

- Do you review whether treatment is in network before I start?

- If biomarker testing is needed, how is that submitted and tracked?

- Can someone help me understand likely out-of-pocket costs?

- What records should I bring so your team can move quickly?

For patients exploring one option among several, Hirschfeld Oncology works with insurance approvals, case management, and access questions related to complex oncology care in an outpatient setting. That matters most when speed and documentation are both important.

The most prepared patients aren't the ones who know all the insurance terms. They're the ones who arrive with their card, their denial letters if they have them, and a short list of direct questions.

If you're looking for practical help with treatment access, insurance questions, and next-step planning, Hirschfeld Oncology offers educational resources for patients and families navigating complex cancer care in New York City.

.png)

.png)